We have all sat through the details of our families’ and friends’ vacation photos (and they, in return, have seen ours).

It’s a rite of passage (so to speak).

I not only enjoy these experiences – because it makes my friends and loved ones happy – I even get inspired to discover new travel destinations.

With summer finally here, I think it’s time to lay out ground rules about why travel insurance is the first stop on my pre-vacation.

Don’t yawn. Informed travel insurance decisions could actually save your retirement (or potentially even your life).

A client of mine – I’ll call him Indiana Jones – had spent years dreaming about the perfect retirement sendoff: A two-month bucket-list expedition through the Amazon rainforest with his equally adventurous wife, who I like to call, Lara Croft.

With puddle jumper jungle planes, communal Amazon boat travel, canoe trips up tributaries, and nights in treehouse-style eco-lodges, their itinerary was a masterclass in advanced adventure travel planning.

But as can happen, just days into the Rainforest, some contaminated water brought the entire trek to a screeching halt.

Lara began experiencing sharp abdominal pains, nausea, and fever. What they hoped was a minor stomach bug worsened (it turned out to be Giardiasis – an awful, waterborne parasite common in regions like the Amazon), and eventually became unbearable.

This, of course, was no joke.

Unfortunately, without access to roads or healthcare, the only option was an emergency medical airlift to a hospital in Manaus, Brazil.

Lara spent three days in the hospital, and they had to cancel the rest of their prepaid eight-week adventure.

The evacuation alone cost over $40,000.

The great news is that, not only did Lara completely recover (they laugh about it now and encouraged me to use their experience as a reminder), but that they also had the foresight to purchase comprehensive travel insurance.

The policy covered the air evacuation, hospital costs, and even reimbursed their unused travel expenses.

How Experiences Like This Should Help You Prepare to Travel

I like a little adventure with my … adventure. And with natural disasters, bankrupt airlines, political unrest, transportation employee strikes, overbooked flights, and random injuries and accidents, our family has been thrown its share of curveballs.

Simply, you do not have to be in the middle of Mongolia’s Gobe Desert to benefit from travel insurance.

Two examples:

We were flying from Italy to France when the regional airline oversold the flight and booted us from our seats. The airline put us up in a hotel and rebooked us the next morning, but we missed our connection back to the U.S.

Since the missed flights were not with the same airline, we were on the hook for entirely new (and last-minute) tickets.

But we had travel insurance. And, thankfully, we filed a claim and recovered almost $1,200 from our provider.

The Ice-Van Cometh

On another trip, while stopped, we slid off an icy road in … Iceland. The tow back onto the road put a big scratch on the vehicle that we failed to notice until we were back at the rental agency.

What could’ve cost us thousands of dollars was covered by our travel insurance, instead.

What Should Your Travel Insurance Cover?

While you can tailor it to cover a wide variety of potential mishaps and worries, here are the core protections that you may want to include in your travel insurance umbrella:

- Protect Yourself from Cancellations or Interruptions

You’ll want to make sure you are eligible to be reimbursed for any prepaid and nonrefundable expenses if you need to cancel or cut your trip short because of illness, injury, a death in the family, or a natural disaster (you may need to provide proof of the event, such as a hospital report). - Get Trip Medical Coverage

Make certain you are protected against healthcare costs if you get injured or sick abroad. (This is especially important if you are over 65 and traveling outside the U.S., because Medicare doesn’t travel with you.) - Insure Yourself Against Baggage Loss, Damage, or Delay

You may be traveling with many thousands of dollars in personal items, including jewelry or, say, a CPAP machine. This reimburses you if your bags are stolen, lost by the airline, or, in some instances, even delayed for a significant period that impacts your travel. - Delays or Missed Connections

This arm of coverage pays for accommodations and related expenses if your flight is delayed or you miss a connection due to covered events. (Friends recently had to pay $2,200 for flights and $400 for a hotel when they missed their connection in Mexico City.) - 24/7 Assistance Services

Often overlooked, there aren’t many things more frustrating than standing at a crowded gate in a foreign country trying to rebook a flight with an overworked attendant who has zero motivation to help you. Reputable travel insurance will include an 800-number with 24/7 support for rebooking flights, locating hospitals, replacing lost passports, or arranging emergency cash transfers.

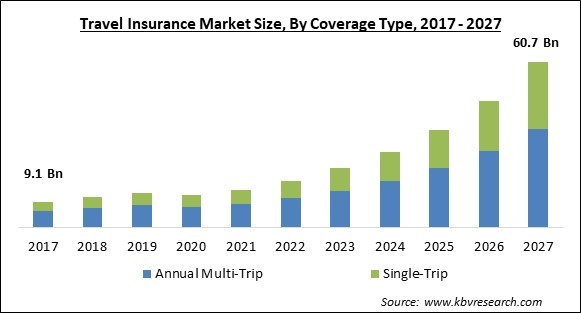

Per-Trip Coverage or Annual Travel Insurance: Which is Best for You?

Did you know that you can buy travel insurance “in-bulk?” This is insurance that covers you, not just for a single trip, but for a year (or even longer).

Per-trip travel insurance is ideal for those folks with one big adventure planned in the future, while multi-trip plans can be cost effective for frequent travelers and snowbirds.

As you can see below, investment in both types of travel insurance, per-trip and annual, are skyrocketing in popularity.

Special Considerations for Travelers Over Age 65

Have you taken 65 trips around the sun? Here are some travel tips that you need to consider.

- Medical Coverage Is Crucial: Much to the chagrin of millions of frustrated travelers, Medicare doesn’t offer coverage abroad (except in limited circumstances). If you are traveling abroad, and are over 65, a robust medical plan is non-negotiable.

- Age-Based Pricing: Unfortunately, premiums rise when you get older, so you should expect to pay more after 65, with another bump after 70.

- Pre-Existing Condition Waivers: Some plans cover pre-existing conditions if purchased within a set time (usually 14-21 days) after your first trip deposit.

- Evacuation Services Matter More – And Are Incredibly Expensive: Older adults are more likely to need medical transport in the event of a serious health issue overseas. Private, international, air-ambulance flights can be as much as $200,000.

What Does Travel Insurance Actually Cost?

So, down to the nitty gritty of what travel insurance could cost you.

On average:

- Per-trip plans are 4% to 10% of total trip cost. Example: For a $10,000 trip, expect to pay $400–$1,000.2

- Annual plans cost $200 – $2000 per year.2

So, generally, the out-of-pocket expense varies based on things such as:

- Your age

- The total cost and duration of the trip

- Destination (the more far-reaching (or isolated) your destination, the higher the fee)

- Desired medical coverage (better too much than too little)

- Optional add-ons (The option to cancel for any reason, rental car coverage, medivac, or medical repatriation flights, etc.)

ProsperPlan Tip

As your advisor and partner in planning, if you’re preparing for a major trip this year, my ProsperPlan co-founder, Chris Grellas, CFP®, MSFA, or I, would be happy to help evaluate your travel insurance as part of your broader financial plan.

We’ve both seen firsthand how the right policy has saved clients tens of thousands of dollars after something unexpected happens.

In short, before your next trip, please don’t hesitate to reach out. We’re happy to help you compare coverage options and integrate them into your risk management plan.

That’s all for now. Best to you! And thank you for your loyalty to Chris, me, and the entire team at ProsperPlan Wealth.

2 How Much Does Travel Insurance Cost? 2025 – Forbes Advisor