Here’s something our clients who have yet to retire often ask:

“Will Social Security be there when I stop working?”

Does that sound like something you’ve wondered?

It’s a question that is borne of fear brought about by an abundance of alarming headlines combined with an information gap about how the system actually works.

And while no one can predict the future, most of the concerns about this important program are not based in fact.

So, with that in mind, I am going to delve into the “big” Social Security question in a way that I believe will alleviate some of your worries.

First, Social Security was Designed to Survive

Social Security was launched in 1935 at the height of the Great Depression; an era when poverty among the elderly was near 50% and unemployment had gotten as high as 25%.

Now, to be sure, the program was never designed to make you wealthy. It was, to be blunt, created to make getting older less cruel by ensuring that people who could no longer work could afford to eat.

And, for the most part, that is what’s happened.

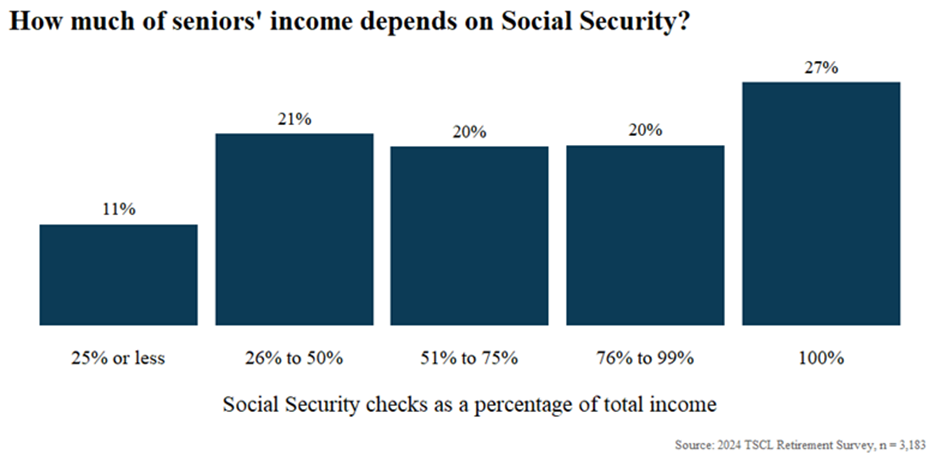

Case in point, according to the Center on Budget and Policy Priorities, a single person is living in poverty if their annual income is below $15,650.1 On its own, Social Security lifts more than 22 million Americans out of poverty annually. And for well over half of all older Americans, the program accounts for 50% or more of their total income.1

This is obviously a good/bad outcome that reminds us how many people struggle to make ends meet once they retire.

Is Social Security going to run out of money?

In theory, yes.

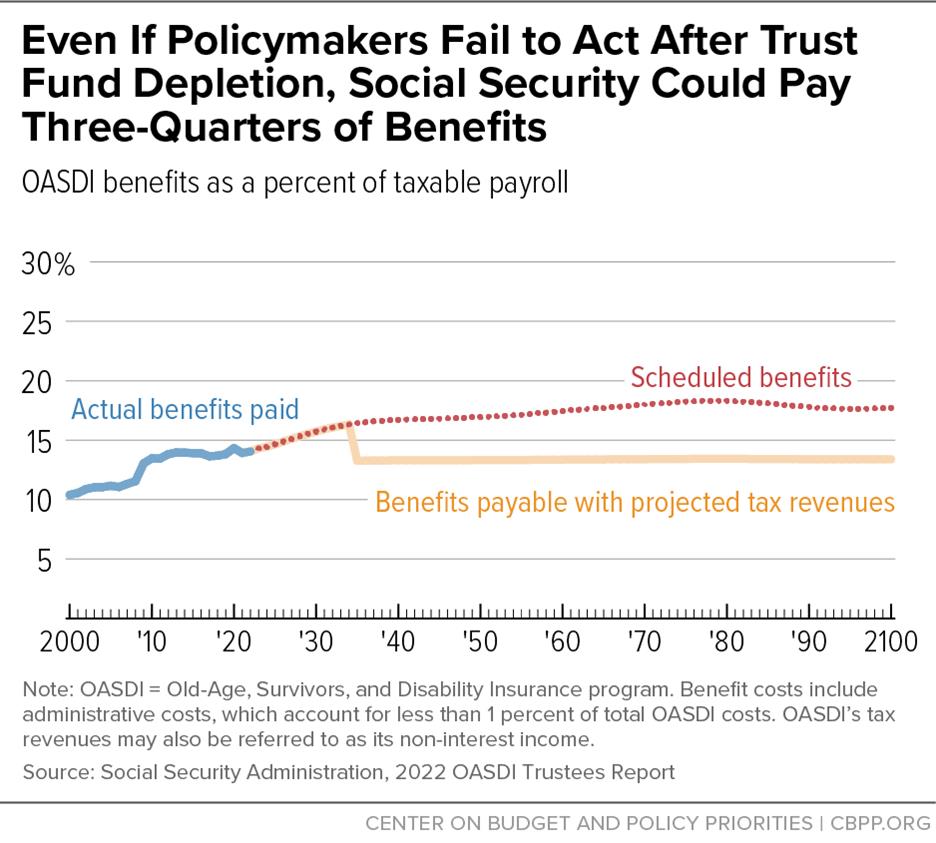

The trust fund (think of it as a reservoir of cash which earns interest) that helps fund Social Security is projected to run dry in roughly a decade, which is something the latest Social Security Trustees’ Report and numerous Congressional Research Service (CRS) white papers have acknowledged.

But what often gets lost is this key detail:

Even if the trust fund is entirely depleted, projected future payroll taxes will still cover about 77% of scheduled benefits.

Of course, that’s a cut, and while alarming, it’s not a collapse. But importantly, those reports aren’t considering the fact that Congress has the time and the authority to fix the program in the interim.

Why is there so much fear that Social Security is going to just go away?

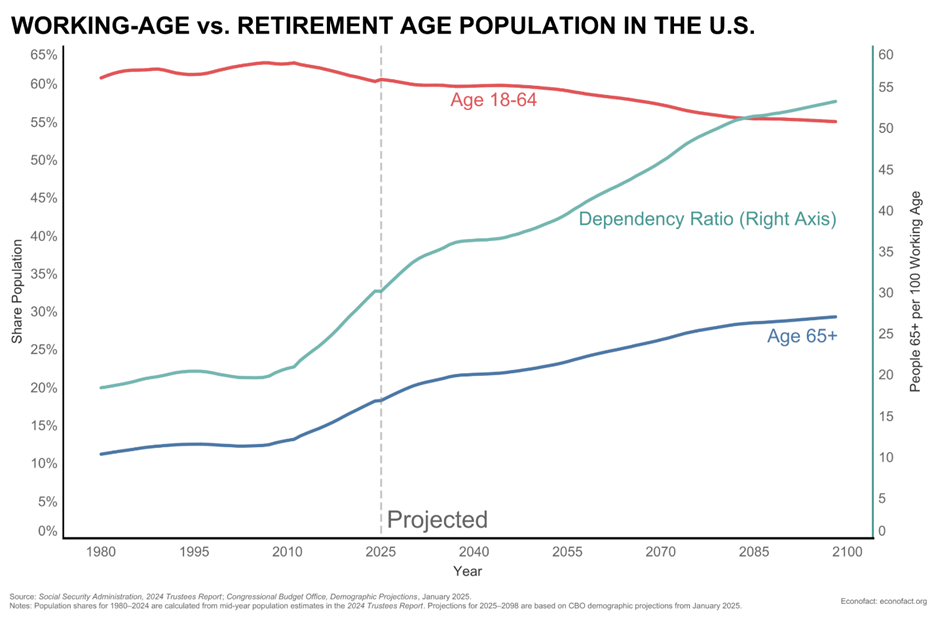

The reality is, that the fear Social Security will just run out of money and “go away” is based more in psychology than hard economics. In a climate of political gridlock, rocketing levels of debt, and shifting demographics (the average age of our population is rising fast), many people feel what can only be described as a low-grade panic about whether anyone is still minding the store.

Below is a commonly distributed graph depicting a potential future where Social Security recipients outnumber those who are paying into the program.

But we’re all adults here, and from debt ceilings to getting laws passed, we all know that, at least historically, when it comes to our government, reforms usually happen just in time.

Some of you may remember that back in 1983, Congress passed a bipartisan package that stabilized Social Security for decades. And most experts, as well as all of the members of our team at ProsperPlan, expect a similar flurry of fixes at some point in the next few years, especially given the dire political consequences if those in charge just sit on their hands.

Plus, despite the concern, even the most severe fixes aren’t nearly as radical as we’ve been led to believe.

As Brookings Institution economists have noted, the approaches to keeping the program whole will probably include:

- Increasing the payroll tax cap (currently $176,000) so that high earners pay more into the system.

- Gradually raising the full retirement age (this would be painful, but is not likely to be implemented anytime soon, nor impact people who are currently within 10 years of retirement).

- Slightly modifying cost-of-living adjustments (COLA) or benefit formulas for the wealthiest retirees.

While certainly not painless, especially to many of you reading this, these are the financial equivalents of steering a large ship a few degrees to avoid an iceberg, and not a call to abandon the ship altogether.

Just for reference, what have some other countries done?

For better, or worse, most Western countries (and Japan) have substantially more robust retirement systems in place than the U.S. currently does. And as the average age of the populations of many countries around the globe has also gotten progressively older, many governments have already started adapting.

Here’s a few examples that my ProsperPlan co-founder, Chris Grellas, MSFA, CFP®, came up with that he found interesting.

Sweden: Often cited in World Bank white papers as a model of reform, Sweden shifted its entire system to a “Notional Defined Contribution” (NDC) plan as recently as 1998. With individual accounts for each person, it closely mimics our own 401(k) plan but still guarantees a minimum benefit.

It’s a bit of a hybrid that balances sustainability with security.

Australia: The Land Down Under added a mandatory superannuation (a regular payment made by workers into a fund) system in the 1990s, which requires employers to contribute to private retirement accounts. Interestingly, this has created one of the largest pension fund markets in the world.

United Kingdom: Great Britain introduced automatic enrollment in private pensions alongside their public pension, which dramatically increased participation among younger workers. (Some of you may work for companies that “auto-enroll” you in their 401(k) plan.)

Japan: With one of the oldest populations on earth, economists have been watching Japan’s retirement planning evolution for decades. In 2000, the Japanese reformed their entire pension system (with major tweaks in 2020) by indexing benefits to population growth and inflation. While these changes haven’t been seamless, nor met with approval by all Japanese citizens, they do at least prove that even aging, highly structured societies can adjust.

The recurring theme for these countries, and for the U.S., is that no one has, nor is any country likely, to throw away the financial safety net for its older citizens. They’re merely reinforcing it through creative, and sometimes difficult, policy decisions.

Why It Still Matters, Especially for Wealthy Families

As a reader of the ProsperPlan newsletter, while it’s almost certain that Social Security isn’t (or won’t be) your primary retirement source of income, it still plays a powerful and significant role.

It’s guaranteed, inflation-adjusted income, and it can act as a buffer during volatile markets. And for couples? It provides survivor benefits, while for those who retire early or live longer than expected, it provides a critical layer of protection.

And further, from a behavioral standpoint? Social Security provides peace of mind, which is one reason why so many people worry about its survival.

There’s just something deeply reassuring about knowing a monthly check will land, no matter what the market or Congress does next.

Also, we have built plenty of our client plans without Social Security as a consideration. But when you’ve qualified for the program and that day arrives?

It not only adds flexibility, strength, and insurance, it’s affirming in a way that is hard to quantify.

The Bottom Line

Social Security isn’t going to be extinct. Slowly, awkwardly, and politically, it’s evolving.

And if there’s anything the global retirement landscape has shown us, it’s that these complex systems can be adapted and preserved.

Because dignity for older Americans is a universal value.

The future of retirement is not a guessing game. It’s a puzzle we help you solve—one thoughtful decision and reform at a time.

That’s it for now. Please reach out to us if you have any questions.